Explore 15 Difference between Sacrificing ratio and Gaining ratio

Sacrificing ratio and gaining ratio are important concepts in accounting and partnerships. They represent different aspects of redistributing profits and losses among partners when there are changes in the partnership structure. While they are related, they serve different purposes and reflect unique aspects of the partnership’s financial dynamics. Let’s explore the fifteen key difference between sacrificing ratio and gaining ratio in simpler terms for better understand.

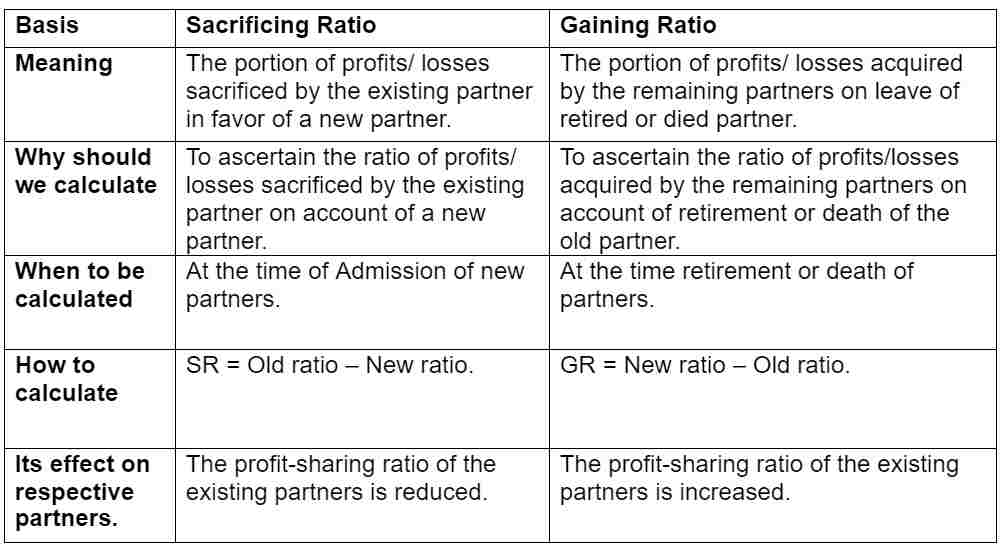

Difference between Sacrificing ratio and Gaining ratio

The sacrificing ratio and gaining ratio both serve to determine how losses are allocated among current partners, as well as how profits are shared.

Calculation: To determine the sacrificing ratio, divide the withdrawal from the partnership by the total sacrificing share. To determine the gaining ratio, divide the partnership’s share of the gain by the total gaining share.

Nature: The redistribution of losses is the subject of the sacrifice ratio, which demonstrates partners’ willingness to bear losses in accordance with their agreement. On the other hand, the gaining ratio describes how partners split increased profits and includes the sharing of profits.

Adjustments: While the gaining ratio may be changed whenever there is a change in the profit-sharing agreement, the sacrificing ratio only applies during the admission or retirement of a partner.

Financial repercussions: Existing partners’ capital accounts are impacted by the sacrificing ratio, which determines how they bear losses. The gaining ratio affects how profits are allocated, deciding how surplus funds are distributed among partners.

Capital contribution: The allocation of losses is impacted by the sacrificing ratio, which takes partners’ capital contributions into account. Gaining ratio, which calculates partners’ individual shares of increased profits, is based on the profit-sharing agreement.

Treatment of goodwill: Since the sacrificing ratio primarily deals with losses, goodwill is not taken into account. Gaining ratio, however, takes goodwill into account because it affects how profits are divided, which is affected by goodwill value.

Asset and liability valuation: While gaining ratio typically does not call for such revaluation, sacrificing ratio may require it in order to determine loss distribution.

Sacrificing ratio can result in changes to partners’ capital accounts, which could have an impact on their ability to maintain their financial stability within the partnership. Gaining ratio controls how profits are distributed but has no direct impact on capital accounts.

Partners’ agreement: The ratio of sacrifices is based on the partners’ agreement to share losses. The partners’ mutual agreement on profit-sharing determines the gaining ratio.

Impact on retiring partners: The amount of losses that retiring partners must bear is determined by the sacrificing ratio, which affects their final settlement. Since it deals with profit-sharing among current partners, the gaining ratio is irrelevant to retiring partners.

Capital adjustment: Depending on the agreed-upon loss-sharing arrangement, sacrificing ratio may require adjustments to the capital accounts of the partners. Unless profit-sharing agreements change, a gain ratio usually does not require capital account adjustments.

Future factors: Depending on the terms of the agreement, the distribution of future losses among partners is impacted by the sacrifice ratio. Depending on the established sharing ratios, the gaining ratio affects how future profits are distributed among partners.

Transferability: Sacrificing ratios cannot be carried over when partnerships or partnership agreements change. Gaining ratio can be moved among various profit-sharing arrangements or partnership structures.

Legal repercussions: If specified in a partnership agreement, the sacrificing ratio has legal repercussions when calculating each partner’s share of losses. Gaining ratio, which is associated with profit-sharing, has legal ramifications for how surplus funds are distributed among partners.

Understanding these difference between sacrificing ratio and gaining ratio helps navigate the complexities of partnership accounting, partnership restructuring, and profit-sharing arrangements with clarity and confidence.